Dabur India is set to continue growing with the growth of the Ayurveda Industry. A market leader in the Ayurveda space, the company looks like a compelling buy with its diversified portfolio, and growth plans. Dabur has grown its market share and volumes amid tough market environment, and high competition. The focus on bolstering its innovation pipeline, especially in natural segment, and premiumising the same is helping the company gain share in the increasing pie of naturals and ayurveda, and also aiding margin improvement.

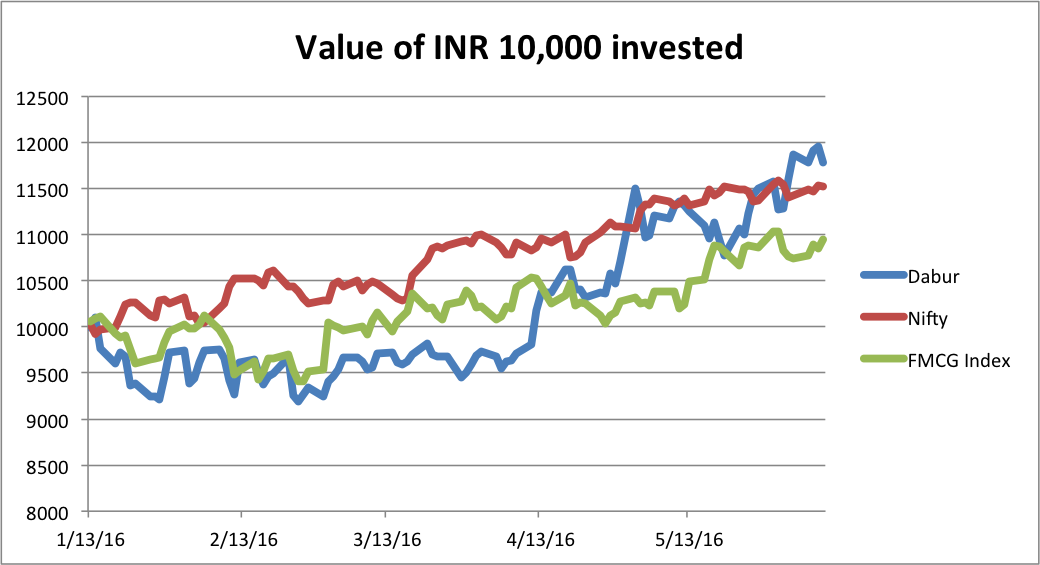

I recommend buying Dabur on dips and holding it for a very long period of time and letting the money grow.

That is, until Patanjali goes Public (jk)

Note: There are no immediate catalysts, so if you’re the one to check the stock price every day, you might want to pass on this one.

Price target over a two-year time horizon:

Target: 395

Upside: 32%

Best Case Scenario: 460 (53% upside)

Worst Case Scenario: 334 (11.3% upside)

Company Overview:

Dabur India Limited is a fast moving consumer goods (FMCG) company. Dabur has two divisions in India: Consumer care division and Foods division. Consumer care division offers a wide range of products in hair care, oral care, health supplements, digestives and candies, baby and skin care products based on ayurveda, over-the-counter (OTC) products, Asavs, and branded ethical and classic products. The Foods division produces fruit juices, cooking pastes, sauces, and items for institutional food purchases.

International Presence: The Company sells its products in domestic as well as international markets. Currently Domestic markets form 68% of revenue and international constitute the other 32%.

The company has acquired two international companies in the past, Hobi (Turkey) and Namaste (USA) to increase its international presence. Over the years, it has expanded its reach internationally, growing business organically as well as inorganically.

There is still a lot of opportunity in the international space with the increasing awareness about Ayurveda.

Competitive Positioning: It must be noted that Dabur is the largest producer of Ayurveda Products in India.

It currently has significant market share and rank in all product segments.

Source: Investor Presentation

With popular brand names such as Real Fruit Juice (55% market share) and Vatika (17% market share), to name a few, Dabur is a leading brand in all verticals.

FMCG Sector overview:

The current size of the FMCG market is 45 Billion. The FMCG sector has grown at an annual average of about 11 per cent over the last decade. The overall FMCG market is expected to increase at (CAGR) of 14.7 per cent to touch US$ 110.4 billion by 2020, with the rural FMCG market anticipated to increase at a CAGR of 17.7 per cent to reach US$ 100 billion by 2025. Growth drivers in the sector are rising disposable income, increasing penetration and consumption and evolving consumer lifestyle. According to Neilson, Dabur, Marico and Baba Ramdev's Patanjali Ayurved are driving the growth in the FMCG space.

Source: IBEF

Since Foods and hair care are leading segments for Dabur as well, growth in the FMCG sector, will have a major impact on top line.

Ayurveda Industry Overview:

The Indian Ayurveda market is currently INR 25,000 cr.

At a global level, Ayurveda products are in great demand. The World Health Organization has projected that the market will reach $5 trillion by the year 2050. Presently, the total turnover is around $62 billion; with India and China being the major players.

In India, the Ayurveda industry is comprised of organized and unorganized sectors that function to cater to the needs and demands of the populace. The organized sector is controlled by major players like Dabur, Zandu, Himalaya, Vicco Laboratories, where they play a vital role in promoting Ayurveda both in the domestic and the international markets. The unorganized sector is run by small Vaidya (Ayurveda experts) families or micro units, who have traditionally been in this field.

The government of India has been taking adequate steps to promote the industry. The government set up the Ayush (Ayurveda, Yoga, Unani, Siddha and Homeopath) Ministry in 2014 to promote the industry.

Dabur is expected to benefit from this market expansion because of its strong product portfolio and a nationwide distribution network.

Investment Trends:

Launch of new products

Dabur has a selective approach towards new launches. Given weak market growth trends, Dabur plans to introduce new products, which have a niche positioning and have a higher probability of consumer acceptance. Some of the recent launches include Real VOLO (aerated fruit beverage), Real Mausambi variant and Honey fruit spreads. These product launches strengthen Dabur’s presence in the FMCG market and because these products are premium, they compete well with MNC players.

Dabur is incubating 200 products, some of which are planned for launch over the counter.

Move towards Ayurveda

Currently, Dabur derives ~60% of it’s revenue from Ayurveda products. Dabur has set itself a target of generating 75 per cent of its revenue in India from products based on Ayurveda by 2020. The move follows the surging popularity of Ayurveda and herbal products in the country and increasing competition from rival brands like Patanjali.

The company plans to increase sourcing medicinal herbs, expand capacity, develop formulations and renew brand promotion to make this possible.

The majority of Dabur’s forthcoming launches, including its baby care portfolio, will be based on Ayurveda. After launching Dabur Baby last year, the company is planning to launch soap, shampoo, body talc and oil. Ayurveda-based baby care would help Dabur differentiate itself from market leader Johnson & Johnson and challengers like Hindustan Unilever.

Expansion plans

Dabur plans to double its herb cultivation as it plans to launch newer ayurvedic products amid growing demand and increasing competition from Pantanjali.

Dabur is setting up its biggest greenfield plant in Tezpur in Assam to manufacture two-thirds of the company’s products. The company is investing Rs 250 crore in the plant, which should be operational by next March. This plant will cater to markets in the northeast, east and north.

The company will then have 3,800 acres of medicinal herb farms by, its fastest expansion so far. At present, it has nearly 2,000 acres under cultivation.

"We are preparing ourself for the next cusp of high demand as our volume growth is still high, partly due to promotions," said Sunil Duggal, CEO at Dabur.

Apart from herb cultivation, Dabur is planning to invest another INR 250 crore in other projects.

Around 100 crore will be invested in building a factory in Uttaranchal. Another 100 crore will be incurred in expanding the company’s international business.

Dabur is also finishing up the expansion operations that it undertook in Patnagar, Uttarakhand. The plan will become operational by January 2017 and is expected to make Dabur self-sufficient in India for supply of juices. Earlier, 60 per cent of juices sold by the company were sourced from its plant in Nepal, where political unrest led to a Rs 100 crore dip in sales in September-December 2015.

These expansion plans will allow the company become self sufficient, and remain competitive. Over the next few years, it drive the top line.

Demand from rural markets

Dabur is set to benefit from recovery in rural growth, which contributes ~45% to total sales, helped by rural-centric initiatives announced in Budget 2016 and likely good monsoons (forecasts indicate good monsoon in FY17).

The company has undertaken initiatives to increase distribution in these areas. Project Double was an initiative rolled out by Dabur in FY13 to expand direct coverage in rural markets

Direct Village coverage has increased from 14000 villages in FY11 to 44,000 villages in FY15. Earlier, this programme was through outsourcing, which will now be done in-house, which will likely increase its efficiency.

The company has also hired a new sales force of 1,000 personnel, which will bolster distribution.

Ban on fixed dose combination drugs

Dabur’s Honitus is positioned for growth as an alternative to other cough syrup, many of which have been banned by the government, as part of its clampdown on fixed-dose combination drugs.

Dabur, could cash in by pushing their products into the vacuum created in the market by the ban.

Source: Economic Times

Development of E-Commerce Platform

Dabur is planning to start an online platform where it will sell products of other companies, along with its own. The platform is likely to go live next year. The fast-moving consumer goods (FMCG) major would sell ayuveda-based health care products, along with providing information on ailments and therapy.

FMCG is expected to follow ticketing, electronics, and fashion categories in e-commerce. A recent study by CII and Boston Consulting Group (BCG) states that by 2020, more that 150 million consumers in India would be digitally influenced. Various studies have predicted the Indian e-commerce market to touch a size of $100 billion by 2020 from around $13 billion at present.

Currently, ecommerce accounts for just two percent of the retail sector. But, it is estimated that it will grow to almost 11 percent by 2019.

Dabur, with its online platform would be poised to take advantage of this opportunity.

The company, which has ventured into online cosmetics and beauty products through NewU, run by its wholly owned arm H&B Stores, is also working on another platform DaburUveda.com to enhance its presence in the e-commerce space.

"We do see that e-commerce is going to expand in a very big way. Thanks to technical development and increased mobile phone penetration, the e-commerce opportunity is going to be very very big. We feel that it is going to expand further in the middle and long term scenario”, said Dabur India CEO, Lalit Malik.

The company already has a well-developed platform: https://www.liveveda.com

Growth in Oral care and Healthcare segments

Dabur's Red toothpaste has muscled its way into the top three toothpastes' charts in the country, riding the herbal Ayurveda wave.

Source: Economic Times

In the most recent quarter, Oral Care performed well with 11.6% growth, led by double-digit growth in the Toothpaste portfolio where Red Toothpaste and Meswak continued the strong momentum driven by consumer advocacy and focused marketing activities. The company’s market share in Toothpaste category reported increase of 200 basis points over same quarter last year. With the current pace of promotional activities, it could be number one within the next few years.

Since oral care forms 16% of FMCG spending, and Dabur derives 15% of its revenue from the oral care segment, continuation of this trend could lead to significant top line growth.

Financial Performance

Dabur’s financial performance has been steadily increasing over the past couple of years.

The company has exhibited solid sales and EPS growth over the past 5 years. Sales have grown at a CAGR of 13% and EPS has grown at a CAGR of 18%.

Current Scenario and Q1 performance

Q1FY17, revenue growth was tepid, 1.1% YoY, due to demand slowdown, amongst other industry headwinds. EBITDA and PAT growth was 8.7% and 11.8% YoY, respectivelyHigher promotions helped volume growth of 4.1% YoY (base of 8.1% YoY), but impacted by PAN card requirement (wholesalers de-stocked in Uttar Pradesh and Madhya Pradesh). Gross margin expansion of 103bps YoY was ploughed back to consumer promotions, while EBITDA margin jump of 126bps was helped by 159bps YoY dip in Ad spends. According to recent conference call, Dabur expects to benefit from renewed focus on herbal and likely rural recovery (45% of revenue) on strong monsoon and rural stimulus. Regulatory challenges related to PAN card declaration (in effect since June’16) affected the wholesale channel adversely in the key North and West markets. Management expects the impact to fade in coming months, though.

Valuation:

Dabur is currently trading at a lower multiple compared to it’s peers in FMCG.

Based on a forward multiple of 40x and an estimated FY18 EPS of 9.8, the price target for Dabur is 395.

Risks:

Key downside risks include: 1) further deceleration in volume growth due to moderation in rural growth (~45% of domestic revenues), 2) increased competition in personal care categories such as skin care, oral care and hair care and/or increased competition in Ayurvedic/herbal space from likes of Patanjali (Honey, Chyawanprash, Toothpastes and Hair Oils are some of the overlapping categories), and 3) any earnings-dilutive acquisitions.